The Raw Steels Monthly Metals Index (MMI) remained sideways, with a modest 0.32% increase from...

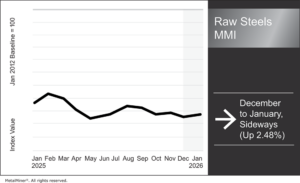

The Raw Steels Monthly Metals Index (MMI) moved sideways with an upside bias, rising 2.48% from December to January.

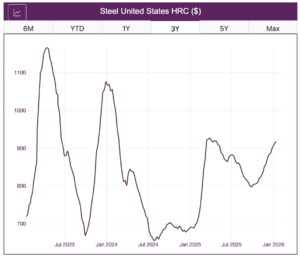

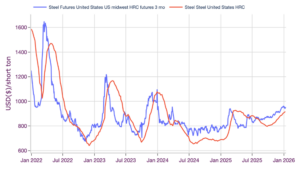

Steel Prices Approach 2025 Peaks

Flat-rolled steel prices continued to trend upward over the last month. HRC, CRC and HDG prices remain decisively bullish, witnessing uninterrupted week-over-week gains. At $917/st, HRC prices sit at their highest level since April, having almost fully rebounded to their March 2025 peak.

Roughly one year ago, incoming tariffs sent the market into a frenzy as buyers stocked up before the duties went into effect at the start of Q2 2025. This resulted in HRC prices peaking at $927/st on March 28 before reversing to the downside over the following two quarters. However, mills regained control over the price trend by the start of Q4, allowing them to tighten supply through maintenance outages and capacity cuts.

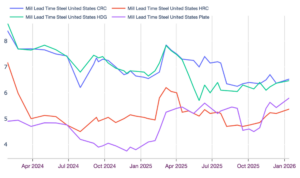

Mill Lead Times Extend

Although overall movements have proven relatively tame, mill lead times are also trending longer. Lengthening lead times suggest a tightening market balance, which will likely support the current uptrend across flat-rolled steel markets.

In contrast to the other forms of steel, plate prices have trended sideways since bottoming out at the start of Q4. Despite this, plate mill lead times are also lengthening, which could prove to be a leading indicator for the plate market.

At the end of 2025, several producers announced price hikes for plate, including Nucor and SSAB. Both producers announced $40/st increases, likely aimed at spurring buying activity. Longer lead times in the market may help these price hikes stick.

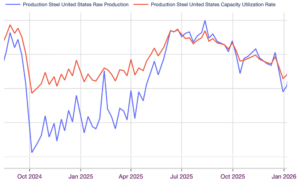

Mill Output Ticks Higher

U.S. steel producers spent the second half of 2025 cutting back output levels in an effort to regain control over steel prices. Maintenance outage cuts in October seemed to stem further price declines. But as lead times largely remained stable over the following weeks, mills were forced to gradually cut output even further to maintain the tight market.

Sources noted slow buying activity at the end of Q4. This comes as the U.S. manufacturing sector closed the year in contraction, with the ISM Manufacturing PMI slipping to 47.9, the lowest reading of 2025.

What’s Next for the U.S. Steel Market?

While 2025 ended on a low note, the market appeared cautiously optimistic for what’s to come in 2026. The Federal Reserve continued to cut interest rates, which is expected to have a gradual, supportive effect on key end-use sectors such as manufacturing and construction.

Though manufacturing remains in a drought, the latest Census Bureau data showed slow increases in construction spending in Q3. While spending remained markedly lower than at the same point in 2024, this nonetheless put an end to the steady declines witnessed throughout most of 2024 and early 2025.

To the mills' advantage, import levels remain decisively slow as tariffs have substantially derailed interest in offshore material among buyers. However, at current price levels, offshore imports of flat-rolled steel are looking increasingly competitive. Should import levels grow, it will likely impede mill efforts to keep the uptrend going.

For now, the bias across all forms of steel remains to the upside, with no indication of any immediate downside corrections. The market remains in contango, with futures holding above spot prices, seemingly supporting a bullish market bias. However, futures appeared to drift lower during the first weeks of 2026. This suggests some caution among investors regarding how much higher steel prices can rise before their next peak.

Biggest Moves for Raw Material and Steel Prices

- U.S. shredded scrap prices posted the largest increase in the index, rising 5.95% to $392 per short ton.

- Chinese coking coal prices rose 5.9% to $159 per metric ton.

- HRC three-month future prices increased 3.37% to $951 per short ton.

- Meanwhile, Chinese slab prices slid by a modest 0.21% to $504 per metric ton.

- LME primary three-month steel scrap prices fell 1.22% to $365 per metric ton.