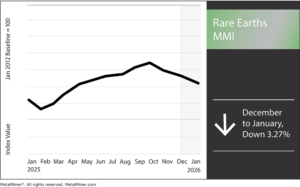

The Rare Earths MMI (Monthly Metals Index) moved sideways, dropping by 2.9%. The rare earths market...

The Rare Earths MMI (Monthly Metals Index) began the year by dropping 3.27%.

As we enter Q1 of 2026, rare earth elements, particularly those used in permanent magnets, sit at the intersection of policy, supply security, and industrial risk.

If you buy rare earths, you’re not purchasing some trivia category on the periodic table. Instead, you’re buying a supply chain that gets stressed at its narrowest point: permanent magnets (NdFeB), plus the specific rare earth inputs that make those magnets strong, compact and durable under heat.

Since mid-December 2025, the macro story has sharpened considerably. While the U.S. is now funding and financing more “mine-to-magnet” capability, the near-term reality still reflects reliance on imports and concentrated processing. That’s the setup for Q1.

Import Reliance Remains the Baseline Risk

The U.S. Geological Survey’s Mineral Commodity Summaries 2025 makes it clear that rare earths remain a U.S. vulnerability. Moreover, the National Defense Stockpile has contemplated acquisitions that explicitly include neodymium-praseodymium oxide and NdFeB magnet forms.

This matters for procurement and finance teams, because the “risk premium” you see in quotes and lead times isn’t just supplier posturing, but the rational pricing of concentration risk, especially for magnet-grade material.

Late-2025 U.S. Policy Shift: Build Capacity and Prove It Can Scale

On December 1, 2025, the U.S. Department of Energy announced a Notice of Funding Opportunity of up to $134 million to strengthen domestic rare earth element supply chains. The DOE’s framing is practical: demonstrate commercial viability for recovering and refining rare earths from sources such as mine tailings and waste streams rather than treating the domestic supply as a long-term science project.

While this won't suddenly flood the market with NdPr or heavy rare earths in Q1 2026, it will change the incentives for processors and off-take negotiations by signaling federal backing for projects that can actually operate at industrial throughput.

Ally-Shoring Becomes More Formal and More Bankable

On October 27, 2025, the U.S. and Japan signed the United States–Japan Framework for Securing the Supply of Critical Minerals and Rare Earths through Mining and Processing.

The language isn’t flashy, but it’s meaningful for buyers. The framework means that both sides have committed to coordinated economic tools and investment to accelerate the development of more diversified and “fair” markets across mining, separation and processing.

For U.S. industrial companies outside the EV/green-energy spotlight (think aerospace components, industrial automation, robotics, medical devices, and high-end electronics), this kind of framework increases the odds that alternative supply channels will become contractable at scale over time.

Permanent Magnets Remain the Chokepoint

One of the most important late-2025 signals for magnet markets came via the U.S. government’s industrial policy ecosystem. Alongside a CHIPS incentive action, the National Institute of Standards and Technology publicly noted a $700 million conditional loan commitment to expand domestic NdFeB magnet production and bolster critical mineral supply chains.

Separately, the Government Accountability Office (GAO) has been blunt about the broader procurement and implementation challenges around critical materials (including rare earth elements) and the need for the Department of Defense to meet statutory requirements.

Put simply: Washington isn’t only talking about “critical minerals.” Rather, it’s increasingly pointing dollars at the steps that determine whether U.S. manufacturers can source magnet-ready material, not just ore.

What U.S. Buyers Should Expect in Q1 2026

- Continued volatility and tighter contracting. With concentrated processing and long qualification cycles, suppliers will keep pushing tighter terms, longer lead times and less flexibility, especially for magnet-critical inputs.

- A gap between “rare earth headlines” and real magnet availability. Even if some upstream pricing cools, the physical bottlenecks can sit downstream in metallization and magnet manufacturing, where capacity takes time to build.

- More CFO-level scrutiny. Boards and finance teams increasingly expect quantified exposure and mitigation planning. The USGS’s reporting and the GAO’s assessments provide credible grounding for those internal risk discussions.

The Bottom Line

The rare earth story entering 2026 represents a managed transition in which the U.S. is funding and financing more domestic and allied capabilities. However, Q1 still carries a risk premium for magnet-linked procurement. Ultimately, the advantage will go to buyers who treat magnets as a strategic category and plan accordingly.

Rare Earths MMI: Noteworthy Price Shifts

- Yttrium prices rose significantly, jumping 14.58% to hit $35.54 per kilogram.

- Dysprosium oxide prices dropped 8.94% to $189.70 per kilogram.

- Terbium oxide prices also fell. Prices dropped 7.95% to $848.68 per kilogram.

- Lastly, rare earth carbonate prices traded flat, remaining at $5124.40 per metric ton.