The Global Precious Metals MMI rose by 4.33% month over month. As of mid-November 2025, all four...

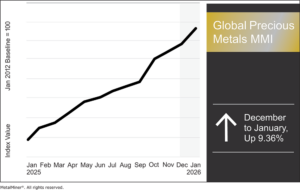

The Global Precious Metals MMI (Monthly Metals Index) once again experienced a month-over-month rise, this time increasing by 9.36%.

Palladium

Palladium still lives and dies by the "automobile" cycle. But in 2026, the focus has shifted away from the automotive market to structural issues in how the market factors risk around supply concentration and benchmark pricing. The Chicago Mercantile Exchange's (CME) outlook frames platinum group metals (PGMs) as behaving more like industrial commodities than monetary hedges, with direct exposure to cyclical auto demand and metal-specific supply constraints.

On the longer-term balance, the World Platinum Investment Council's (WPIC) 2- to 5-year view expects palladium to remain in deficit for 2026, with the market only transitioning to surpluses from 2027 onward. Those surpluses will then build gradually later in the decade. For U.S. automotive procurement teams, that reads as, “don’t count on a clean, straight-line drop.” There will still be volatility, substitution decisions and supplier behavior around tightness versus surplus.

Platinum

Platinum’s near-term story is unusually concrete. The WPIC currently predicts that the 2026 market will “move to being in balance” with a small surplus, depending on specific flows like exchange-stock outflows and ETF profit-taking. That conditionality matters, and U.S. buyers shouldn’t take “balance” to mean “cheap.”

The other platinum headline is "operational.” LBMA’s January 14, 2026 announcement confirms a Q3 2026 transition to IBA administration and explicitly frames the goal as “transparent, robust and rigorous” reference pricing. That’s a credibility point, but it’s also a timing point, underscoring the need to incorporate the change into risk reviews now rather than waiting until the week before implementation.

Silver

Silver is where industrial buyers feel the pinch fastest because substitution options are limited in many electronics applications. The Silver Institute, citing analysis from Metals Focus, indicates that the market is on course for a fifth consecutive year of structural deficits. The organization cites tariff concerns, a liquidity squeeze with record-high lease rates, and ongoing geopolitical risks as reasons for the shortfall.

Crucially, the same work quotes Metals Focus Managing Director Philip Newman in the context of the Silver Institute’s New York industry discussions. This ties the deficit narrative to real market structure rather than “vibes.” For U.S. electronics and automotive-electronics buyers, that’s a classic “even when demand dips, the market can stay tight” setup.

Gold

Gold is the "CFO metal" for a reason. The CME flags central bank accumulation as a structural factor likely to remain relevant in 2026 as it continues shifting the demand base toward longer-term holders. Meanwhile, World Gold Council (WGC) data puts numbers to that sentiment. Marissa Salim, Senior Research Lead at the WGC, reports net central bank gold purchases of 45 tons in November 2025, bringing total purchases to around 297 tons as of January that year.

For U.S. buyers, gold’s industrial role is smaller than that of silver or PGMs. However, its signal is loud and clear. If central banks keep accumulating and correlations shift, gold can stay expensive even when traditional “real yield logic” gets messy.

Global Precious Metals MMI: Noteworthy Price Shifts

- Palladium bar prices rose 12.32% to $1,604 per troy ounce.

- Platinum bar prices increased 23.27% to $2,066 per troy ounce.

- Silver ingot prices rose 26.60% to $71.54 per troy ounce.

- Finally, gold bullion prices moved sideways, dropping by 1.99% to $4,317.60 per troy ounce.