The Automotive MMI (Monthly Metals Index) moved sideways, rising by a modest 2.48%. Recent...

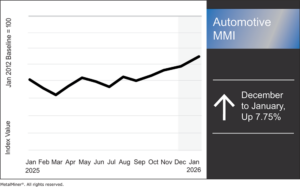

The Automotive MMI (Monthly Metals Index) moved up by a significant 7.75%.

From mid-December through mid-January, the U.S. automotive market sent a clear signal to metal buyers that prices are holding firm. This comes even as vehicle demand shows signs of stabilizing rather than surging. For OEMs and Tier 1 suppliers, this period underscored a structural shift that has been building for years.

Steel Pricing Remains Sticky as Tariffs Set the Floor

The U.S. government’s June 2025 move to raise Section 232 tariffs on steel and aluminum imports from 25% to 50% remains one of the most important structural inputs for automotive metal costs. The White House laid out the rationale and effective date in its June 3, 2025 fact sheet, with the increase taking effect on June 4, 2025.

The Congressional Research Service also summarized the change, including key carve-outs (such as the UK) and the broader way in which the policy limits import competition for domestic producers. For automotive buyers, the implication is straightforward: domestic steel benchmarks now have an artificial support level. This means tariffs limit how much cheaper imported steel can be, which, in turn, limits downside risk for U.S. mill pricing even if vehicle demand softens.

Automotive Aluminum Risk is Concentrated in Sheet Supply

Keeping aluminum tightly automotive-focused, the key risk signal since mid-December has been sheet supply concentration rather than generalized aluminum pricing headlines.

Novelis’ public update explains the September 16, 2025 fire at its Oswego, New York facility, outlines mitigation efforts and confirms expectations for the hot mill to return in early Q1 2026. Independent reporting has also highlighted that the incident mattered disproportionately to automakers because the site plays a significant role in supplying aluminum sheet for automotive body applications.

The procurement takeaway is simple but critical. Automotive aluminum sheet remains a concentrated category in North America. Risk management here is less about short-term price movement and more about qualified alternate supply, inventory buffers and contract protections.

Vehicle Sales Finished 2025 Firm, Supporting Baseline Metal Demand

Cox Automotive projected and later reaffirmed that U.S. light-vehicle sales would finish 2025 at approximately 16.3 million units. Despite some cooling in Q4, this represents an improvement over 2024. However, for procurement teams, volume alone does not provide the full story, as vehicle mix matters more than total units. Full-size pickups and SUVs carry significantly higher steel and aluminum content than compact vehicles, which helps to support baseline demand for automotive metals even when headline sales growth slows.

OEM Strategy Signals Are Translating Directly Into Metals Exposure

OEM strategy changes continue to show up first in sourcing requirements. For instance, General Motors’ year-end U.S. sales release underscored strength in full-size pickups and SUVs, both segments with high metal intensity.

These shifts have downstream implications for procurement. For instance, powertrain decisions affect copper intensity, while platform choices influence aluminum sheet demand. Finally, thermal and emissions system changes alter exposure to stainless and specialty alloys. For sourcing leaders, OEM announcements are often early warnings of where pricing and qualification pressure will surface next.

Automotive MMI: Noteworthy Price Shifts

- Chinese lead prices moved sideways, rising by 1.7% to $2,440.54 per metric ton.

- Hot-dipped galvanized steel prices rose 3.96% to $1,103 per short ton.

- Lastly, Korean aluminum 5052 coil premium over 1050 traded flat, remaining at $4.25 per kilogram.