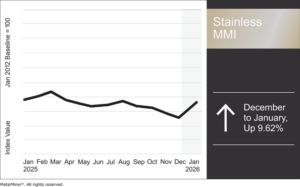

The Stainless Monthly Metals Index (MMI) broke out to the upside, jumping 9.62% from December to January.

Stainless Market Stable, Nickel Prices Spike

The stainless steel market remains largely stable, with little evidence of a meaningful rebound in underlying demand or activity. While the stainless index recently recorded an uptick, the move appears to have been driven primarily by higher raw material costs rather than improving market demand.

By January 7, nickel prices had surged to their highest level since June 2024, lifting the overall Stainless Monthly Metal Index while other components moved sideways. However, nickel prices corrected to the downside in subsequent sessions. This suggests that the recent increase in both nickel prices and the overall index may reflect short-term volatility rather than meaningful trend shifts.

Indonesia Plans Production Cuts

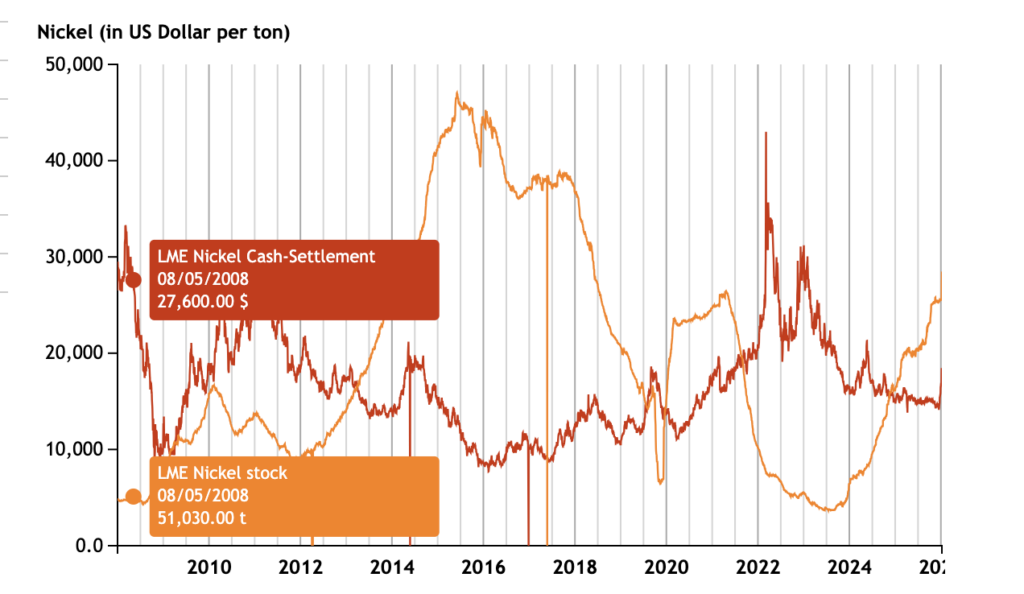

Nickel prices languished throughout most of 2025. Prior to the most recent rally, prices appeared poised to close the year as the worst-performing base metal contract. At the start of December, prices stood at a modest discount to where they closed 2024. However, they soon rebounded to close the year at a modest premium, outperforming lead.

Sliding nickel prices reflected an accumulating supply glut. Demand conditions remained weak for stainless steel and other nickel end-uses, while Indonesian output remained robust. This saw global inventories balloon. Lower prices gradually forced mines outside Indonesia to close due to profitability concerns. However, these cuts did little to impact surplus conditions and, therefore, had no impact on investor sentiment.

By December, Indonesia finally decided to step in. The world’s largest nickel producer, accounting for an estimated 70% of global supply, signaled that it will reduce its nickel output in 2026 by tightening mining quotas and production plans. Both government officials and the Indonesian Nickel Miners Association have indicated that the 2026 Work Plan and Budget (RKAB) could lower the country’s nickel production target to around 250 million tonnes, a 34% cut from the roughly 379 million tonnes planned previously. The move is part of broader efforts by Jakarta to control oversupply, support metal prices and stabilize the market.

High Stocks, Questions Over Cuts Quash Rally

Indonesia’s announcement was long overdue and will invariably support the overall market. However, the spike in nickel prices appears largely reactive, given that many downside risks remain. For one, the market still has to grapple with the build-up of supply. LME stocks currently sit at their highest level since 2021, having risen even further in January as investors capitalized on the recent price spike to offload material.

Additionally, and perhaps most importantly, markets remain skeptical over whether the cuts will occur as planned. Producers are applying significant pressure on Jakarta to soften or reverse the planned quota reductions, arguing that stricter limits could disrupt existing smelter operations and future investment.

In past years, similar intentions to curb output were undermined by the eventual approval of higher quotas than initially proposed. Many expect the government may yet again relent under political and economic pressure. This ambiguity around the final level and the enforcement of quotas has introduced significant uncertainty into the nickel price outlook.

The practical impact of this uncertainty has been notable in price behavior. Initially, markets rallied on the prospect of tighter supply. But without concrete, enforceable quota cuts, the recent gains are vulnerable to an ongoing reversal. Traders continue to remain cautious because the Indonesian policy framework has sometimes fallen short of delivering the anticipated supply constraint. Meanwhile, there are still stockpiles of the metal large enough to offset production reductions in the short term.

So, while the possibility of lower Indonesian output has supported elevated nickel prices, the lack of clear commitment and details has tempered confidence that such a rally can be sustained without firmer policy action.

Biggest Nickel and Stainless Steel Price Moves

- Chinese primary nickel prices witnessed the largest increase of the overall index, soaring 15.78% to $19,603 per metric ton as of January 1.

- Indian primary nickel prices rose 13.48% to $16.95 per kilogram.

- LME primary three-month nickel prices increased 11.76% to $16,630 per metric ton.

- Meanwhile, the Allegheny Ludlum surcharge for 304/304L coil fell 1.32% to $0.87 per pound.

- The Allegheny Ludlum surcharge for 316/316L coil dropped by 4.73% to $1.40 per pound.