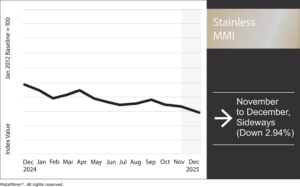

The Stainless Monthly Metals Index (MMI) appeared increasingly weak, sliding by 2.94% from November...

The Stainless Monthly Metals Index (MMI) appeared increasingly weak, sliding by 2.94% from November to December.

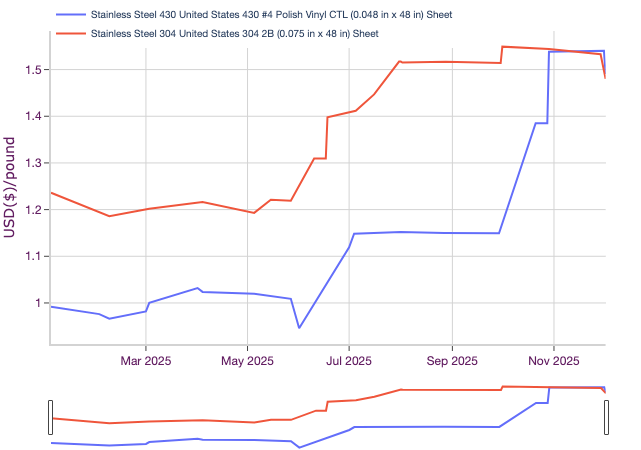

304, 430 Base Prices Trend Lower

Stainless base prices trended lower from previous months as weak demand conditions dragged the market. Base price discount estimates for 304 hit their highest level since July, while 430 discounts hit their highest level since June.

Ahead of Q4, expectations from market participants appeared split. Some anticipated firm pricing and were somewhat surprised by the recent price erosion. They believed that lower import volumes (as a result of tariffs) had given mills considerable control over the domestic market. While demand conditions remained weak, mills had enough leverage to tweak capacity utilization rates, keeping the market tight.

However, others disagreed. One source noted that as stainless steel demand appeared weak globally (not just in the U.S.), the considerable price hikes issued by domestic mills witnessed over the summer would be difficult to maintain. While Outokumpu opted to forgo capacity expansions at the start of the year, North American Stainless will add capacity at its Ghent facility. While they agreed that tariff rates would (and have) substantially trimmed import volumes, oversupply conditions remain a longstanding issue for the market amid the lack of a demand rebound over recent years.

NAS’ decision to delay the official start of the Ghent expansion came as a telltale sign for skeptics of current price levels. Sources noted that the decision to open the facility in Q1 2026, rather than the initial plan to begin production by the end of 2025, was likely not made lightly, given the significant investment.

At the very least, mills were able to keep prices firm for H1 contracting purposes. 2026 contracts will see manufacturers pay significantly higher prices than they did in 2024. Price hikes, which hit the market over the summer months, affected only spot purchases and new business, as manufacturers shifted away from offshore sources. This means that, to date, higher prices have benefited only a small portion of the mill business.

Imports Low and Demand Weak

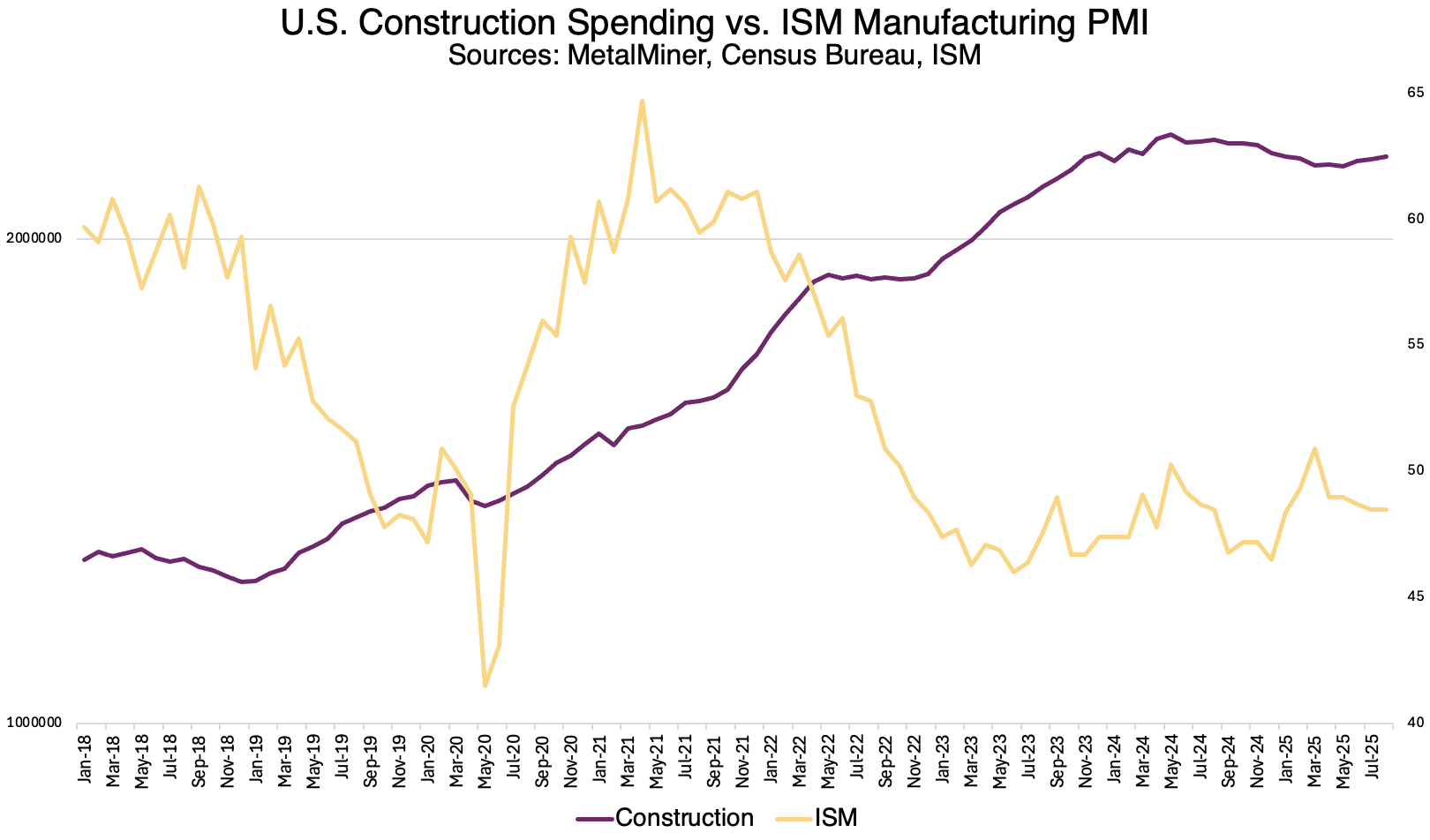

While tariffs have helped U.S. mills considerably, demand has not strengthened. The manufacturing sector has yet to return to growth, trending deeper into contraction over recent months. Meanwhile, even with recent, albeit modest, increases in spending, U.S. construction spending remains considerably lower than where it stood the previous year.

Recent Federal Reserve rate cuts will provide some support to markets. However, when that becomes apparent in major end-use sectors and when that will translate to a rebound in the U.S. manufacturing sector remains uncertain, particularly amid a weakening labor market. The U.S. construction industry will see new demand from U.S. infrastructure efforts and the ongoing growth of data center investments in 2026, but market sources appeared skeptical that this will offset weakness elsewhere in stainless demand.

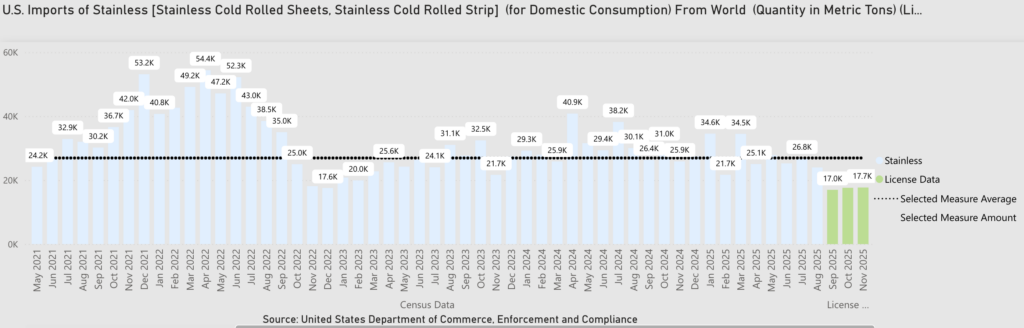

Nonetheless, tariffs have created a higher price floor for the market. Imports are much lower than they were in past years, which means more business for U.S. mills. While lower, the drop appears less drastic than what has been witnessed in markets like carbon steel. At current price levels, there are still opportunities for imports from Asia to enter the U.S. market.

This could mean that stainless steel base prices have further to fall in the coming months. While mill lead times remain stable, NAS’ Ghent facility remains a downside risk next year, even if they are able to introduce that capacity slowly. Additionally, a quota agreement with the EU remains possible. The EU continues to press for tariff relief from the U.S. The U.S. offered to do so if the EU was willing to roll back digital regulations. Thus far, the EU has refused, but this stance could change in the following year.

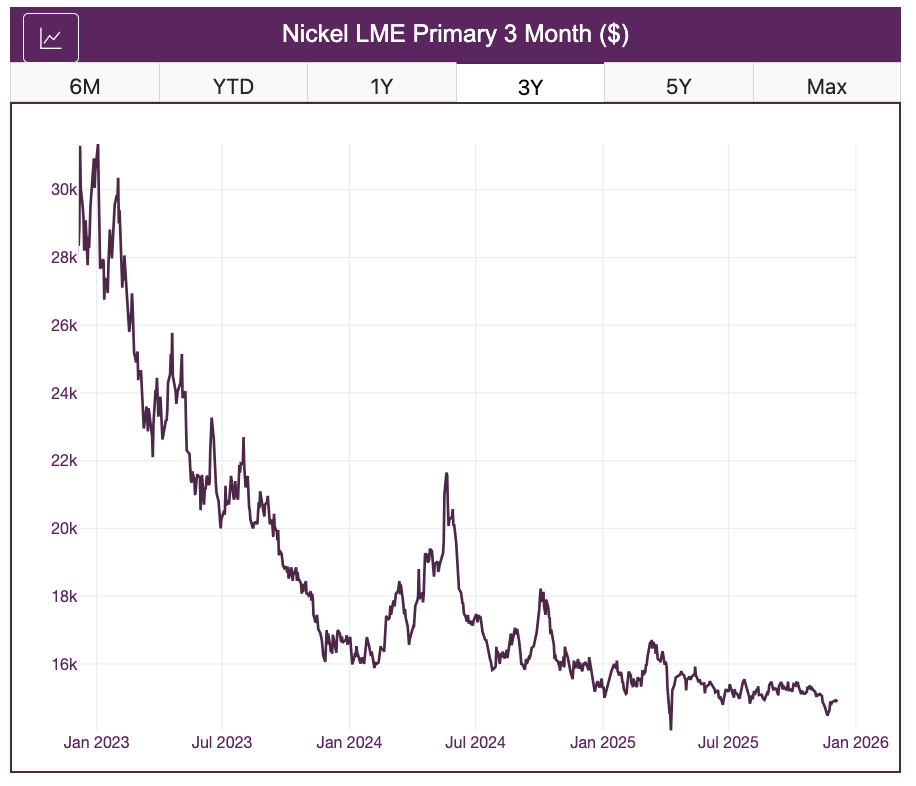

Nickel Prices Set to Close 2025 as Worst-Performer

While base prices are up year over year, nickel prices remain depressed. Prices trended mostly sideways throughout the year before slipping below range in November. The recent decline proved modest, but set the nickel contract up to become 2025’s worst-performing base metal contract. As of December 4, prices have fallen 2.35% from the close of 2024. Absent meaningful declines in lead and zinc prices over the next few weeks, which are currently clocking very marginal year-to-date increases, this will see the nickel contract as the only base metal price to depreciate during the year.

The nickel market remains vastly oversupplied. Despite mine supply cuts, Indonesian production levels continue to translate to a significant supply glut. SHFE and LME inventory stocks sit at multi-year highs. Indonesia has made some efforts to constrain supply, recently slashing its mining quota by 120 million tons, but thus far, those efforts have proven unable to tame oversupply. Until the market changes, the current nickel price floor will remain fragile.

Biggest Nickel and Stainless Steel Price Moves

- Chinese ferrochrome prices witnessed the only increase of the overall index, rising by a modest 0.44% to $1,295 per metric ton as of December 1.

- Meanwhile, the Allegheny Ludlum Surcharge for 316/316L coil slipped by 1.61% to $1.47 per pound.

- LME nickel prices fell 2.23% to $14,880 per metric ton.

- Korean 304 2B cold rolled coil prices declined by 2.81% to $2,269 per metric ton.

- Chinese ferromolybdenum prices dropped by 10.87% to $33,291 per metric ton.